Asset Pricing

Liquidity and Price Informativeness of Options: Evidence From Extended Trading Hours

Journal of Futures Markets, 2025

Liangyi Mu, Arie E. Gozluklu

This paper explores the trading dynamics of the options market during extended trading hours (ETHs). During ETH, the options market is characterized by low liquidity and decreased trading activities, yet there is an increased likelihood of informed trading. The introduction of ETH improves overall market liquidity on the following trading day, as reflected by a reduction in the quoted and effective bid–ask spreads, for both index options and their underlying constituents. The improvement of liquidity is due to the timely incorporation of overnight news into option prices during ETH. Moreover, option prices during ETH are informative for the index level and realized volatility in the subsequent regular trading hours.

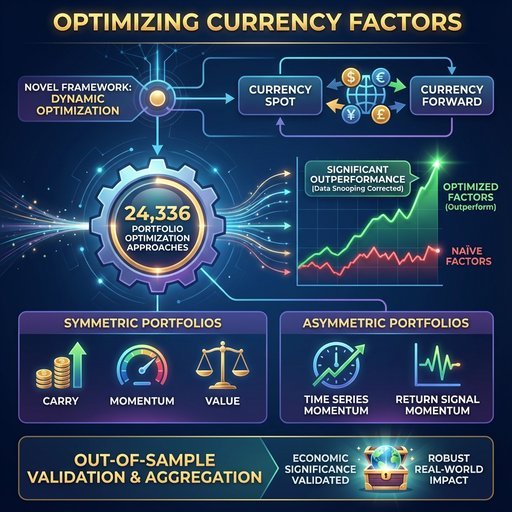

Optimizing Currency Factors

Financial Review, 2025

Minyou Fan, Fearghal Kearney, Youwei Li, Jiadong Liu

We introduce a novel framework that dynamically optimizes currency factor strategies via trading currency spot and forward. We examine the performance of 24,336 portfolio optimization approaches and find that the optimized currency factors significantly outperform the naïve factors after correcting for data snooping bias. Our framework suits both symmetric factor portfolios, including carry, momentum, and value, and asymmetric factor portfolios, such as time series momentum and return signal momentum. An out-of-sample procedure that aggregates all the outperforming optimization approaches validates the economicsignificance of our optimized factor portfolio.

Unravelling the volume-volatility nexus in cryptos under structural breaks using fat-tailed distributions: mixture of distribution hypothesis and implications for market efficiency

European Journal of Finance, 2025

Saswat Patra; Neha Gupta

The study examines the relationship between volume and volatility in leading cryptocurrencies i.e. Bitcoin and Ethereum, within the framework of Mixture of Distribution Hypothesis (MDH). It accommodates structural shifts in the cryptocurrency prices and uses fat-tailed distributions. The results show that the MDH is rejected for both cryptocurrencies, and volume alone cannot explain the heteroskedasticity of returns; however, it acts as a significant predictor for volatility, especially when incorporating structural breaks in the model. Further, the forecasting performance improves when fat-tailed distributions, such as the skewed student’s t and Johnson’s Su distribution are used to model the innovations. Thus, volume holds important information in the crypto markets and can affect returns, thereby, raising concerns about market efficiency. Our results are robust across different periods, modelling approaches and forecasting horizons, and hold substantial implications for traders, market participants, regulators, and governments in designing effective policies.

Understanding the Performance of Currency Basis‐Momentum

European Financial Management, 2025

Minyou Fan, Xing Han, Ang Li, Jiadong Liu

We conduct an in‐depth analysis of basis momentum (BM) in currency markets and examine its relationship with key market anomalies. We find that BM strategies generate significant excess returns across various formation periods. These abnormal returns are not fully explained by the closely related carry and momentum factors. By decomposing the BM signal, we show that both carry‐ and momentum‐related components contribute to the returns of BM strategies. Compared to carry trade, BM strategies exhibit significantly lower risk, leading to superior risk‐adjusted performance.

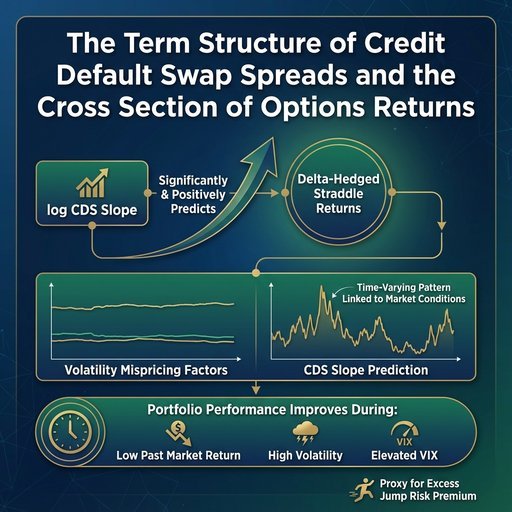

The Term Structure of Credit Default Swap Spreads and the Cross Section of Options Returns

Journal of Futures Markets, 2025

Hao Zhang, Yukun Shi, Dun Han, Pei Liu, Yaofei Xu

This paper, using the natural logarithmic form credit default swap (log CDS) slope, examines the variation in cross‐sectional 1‐month ATM delta‐hedged straddle returns. Our analysis reveals that the log CDS slope significantly and positively predicts these returns, even when accounting for several key volatility mispricing factors. Further investigation shows that this predictive relationship exhibits a strong time‐varying pattern, closely linked to market conditions. In contrast, the relationship between notable volatility mispricing factors and straddle returns remains relatively stable over time. Constructing a long‐short quintile portfolio on straddle options confirms that trading performance improves when the past 12‐month market return is at a historically lower level, market volatility is at a historically higher level, and the VIX is elevated. Log CDS slope, as a proxy for excess jump risk premium, significantly predicts delta‐hedged option returns during periods of high volatility.

Nonstandard errors

Journal of Finance, 2024

Albert J. Menkveld, Anna Dreber, Felix Holzmeister, Juergen Huber, Magnus Johannesson, Michael Kirchler, Sebastian Neusüß, Michael Razen, Utz Weitzel, Fincap Team, Fearghal Kearney, Tony Klein, Liangyi Mu, and others

In statistics, samples are drawn from a population in a data-generating process (DGP). Standard errors measure the uncertainty in estimates of population parameters. In science, evidence is generated to test hypotheses in an evidence-generating process (EGP). We claim that EGP variation across researchers adds uncertainty--nonstandard errors (NSEs). We study NSEs by letting 164 teams test the same hypotheses on the same data. NSEs turn out to be sizable, but smaller for more reproducible or higher rated research. Adding peer-review stages reduces NSEs. We further find that this type of uncertainty is underestimated by participants.

Lurking in the shadows: The impact of CO2 emissions target setting on carbon pricing in the Kyoto agreement period

Energy Economics, 2023

Barry Quinn, Ronan Gallagher, Timo Kuosmanen

This paper is a case study of the impact of CO2 emissions target setting. We empirically investigate the targets set during the Kyoto Protocol period using a convex nonparametric least squares system, quantile regressions, and a comprehensive data set of 125 countries. Our findings reveal CO2 marginal abatement costs, which: (1) are significantly higher for target setting countries; (2) increase over the sample period; (3) and are an order of magnitude greater than the prevailing emissions pricing mechanisms. The results provide insights into the consequences of policies to curb unwanted by-products in a regulated system and shed light on the price efficiency of carbon markets. Furthermore, we contribute to the debate on emission reduction standard-setting and highlight the importance of shadow price estimates when regulating market instabilities in an emission trading scheme.

Macroeconomic news and price synchronicity

Journal of Empirical Finance, 2023

Arbab K. Cheema, Arman Eshraghi, Qingwei Wang

Stock price synchronicity is a critical consideration for asset allocation, risk assessment, and hedging decision. We present novel evidence that individual stock returns comove more persistently on certain days of the week. Specifically, we show that release of macroeconomic news on Mondays, which typically see fewer announcements, leads to such stronger comovement, and that this is distinct from the Monday effect typically discussed in the literature. This synchronicity is more pronounced among large, old and low volatility firms, in both up- and down-market conditions. We argue this effect is partly due to 'simultaneous contrast', i.e., perception of stimulus depending on its surrounding environment. Monday announcements have a larger impact just as thunder in a quiet night sounds louder. Our findings are robust after controlling for day-of-the-week effects, economic uncertainty, risk aversion, investor sentiment, short-selling constraints and proxies for attention to news.

Does geopolitical risk affect firms' idiosyncratic volatility? Evidence from China

International Review of Financial Analysis, 2023

Xiaohang Ren, Yuxuan Cao, Pei Liu, Dun Han

Using 2663 Chinese A-share listed companies from 2003 to 2019, we investigate the relationship between geopolitical risk (GPR) and firm idiosyncratic volatility through panel fixed effects and attempt to explain the mechanism. The main findings are presented as follows. First, GPR can explain the change of firms' idiosyncratic volatility. Different industry conditions and ownerships have heterogeneous effects on the firms' idiosyncratic volatilities. In addition, the interaction terms of ownership concentration, competitive intensity and operating leverage with GPR are statistically significant, and they interact with GPR to affect firms' idiosyncratic volatility. After we conduct a series of robustness tests using methods such as instrumental variables, we innovatively introduce the South China Sea dispute as an external event and use the DID (Difference-in-difference) model to analyze the impact of geopolitical events on corporate risk-taking, our findings remain valid. Our research contributes to a better understanding of geopolitical risk and firms' idiosyncratic volatility.

Order book price impact in the Chinese soybean futures market

International Journal of Finance & Economics, 2023

Muzhao Jin, Fearghal Kearney, Youwei Li, Yung Chiang Yang

We study the price impact of order flow in the world's largest soybean meal futures markets. Our intraday results indicate that incoming orders can be used to explain and predict future price changes. Our results are shown to be robust to various order flow measures, price aggregation approaches and data frequencies. We find that order flow imbalance (OFI) is a more all-encompassing measure carrying greater information about price change relative to both trade imbalance (TI) and volume. Moreover, while both OFI and TI are shown to predict future price changes, this predictability diminishes over longer measure and price change frequency horizons.

Time series reversal in trend-following strategies

European Financial Management, 2023

Jiadong Liu, Fotis Papailias

This paper empirically studies the reversal pattern following the formation of trend-following signals in the time series context. This reversal pattern is statistically significant and usually occurs between 12 and 24 months after the formation of trend-following signals. Employing a universe of 55 liquid futures, we find that instruments with sell signals in the trend-following portfolio ('losers') contribute to this type of reversal, even if their profits are not realised. The instruments with buy signals in the trend-following portfolio ('winners') contribute much less. A double-sorted investment strategy based on both return continuation and reversal yields to portfolio gains which are significantly higher than that of the corresponding trend-following strategy.

Can real options explain the skewness of stock returns?

Journal of Banking & Finance, 2023

Tuan Ho, Kirak Kim, Yang Li, Fangming Xu

We study a novel mechanism through which real options play a prominent role in inducing the skewness of stock returns. Building on the investment-based asset pricing framework, we show that firms' real options to contract (expand) their businesses when productivity is low (high) can increase return skewness. Consequently, return skewness represents a U-shaped function of firm productivity. Furthermore, the real-options effect is stronger for more flexible firms, characterized by lower scale-adjustment frictions. Employing a large sample of U.S. firms during 1972-2018, we provide a battery of robust empirical evidence consistent with the model predictions. Our findings demonstrate that firm-level real flexibility can impact investors and managers' decision making.

Momentum and the cross-section of stock volatility

Journal of Economic Dynamics and Control, 2022

Minyou Fan, Fearghal Kearney, Youwei Li, Jiadong Liu

Recent literature shows that momentum strategies exhibit significant downside risks over certain periods, called momentum crashes. We find that high uncertainty of momentum strategy returns is sourced from the cross-sectional volatility of individual stocks. Stocks with high realised volatility over the formation period tend to lose momentum effect. We propose a new approach, generalised risk-adjusted momentum (GRJMOM), to mitigate the negative impact of high momentum-specific risks. GRJMOM is proven to be more profitable and less risky than existing momentum ranking approaches across multiple asset classes, including the UK stock, commodity, global equity index, and fixed income markets.

Dynamic functional time-series forecasts of foreign exchange implied volatility surfaces

International Journal of Forecasting, 2022

Han Lin Shang, Fearghal Kearney

This paper presents static and dynamic versions of univariate, multivariate, and multilevel functional time-series methods to forecast implied volatility surfaces in foreign exchange markets. We find that dynamic functional principal component analysis generally improves out-of-sample forecast accuracy. Specifically, the dynamic univariate functional time-series method shows the greatest improvement. Our models lead to multiple instances of statistically significant improvements in forecast accuracy for daily EUR-USD, EUR-GBP, and EUR-JPY implied volatility surfaces across various maturities, when benchmarked against established methods. A stylised trading strategy is also employed to demonstrate the potential economic benefits of our proposed approach.

Accurate forecasts attract clients; biased forecasts keep them happy

International Review of Financial Analysis, 2022

Chao Zhang, David G. Shrider, Dun Han, Yanran Wu

We examine whether business relationships between mutual funds and sell-side analysts influence earnings forecasts using Chinese data from 2007 to 2019. Consistent with prior studies, our results support the commission pressure hypothesis. Analysts' forecasts are overly optimistic for the holdings of existing fund clients. Significantly, we propose the potential client hypothesis and show that analysts' forecasts are more accurate for the holdings of funds that are not clients than for holdings of clients or for stocks not held by any fund. Our results suggest that commission pressure from existing fund clients increases analysts' optimistic bias, while potential clients pressure inhibits analysts' optimistic bias to some extent. Finally, our evidence supports the conflicts of interest hypothesis. Commission pressure is reduced as economic uncertainty grows.

Are carry, momentum and value still there in currencies?

International Review of Financial Analysis, 2022

Mark C. Hutchinson, Panagiotis E. Kyziropoulos, John O'Brien, Philip O'Reilly, Tripti Sharma

We show that carry, momentum and value predictability in currencies is associated with mispricing. Specifically, investment performance disappears subsequent to published evidence showing portfolio returns are not fully explained by risk. Replicating these studies, we show that the average out-of-sample Sharpe ratio decreases from +0.39 to -0.32. Cross sectional tests show that currencies no longer respond to interest rate and real exchange rate differentials. During this period currency excess returns do not exhibit autocorrelation. Our results are consistent with investors learning about mispricing from academic research.

A reexamination of factor momentum: how strong is it?

The Financial Review, 2022

Minyou Fan, Youwei Li, Ming Liao, Jiadong Liu

Recent studies show that most financial market anomalies exhibit a momentum effect. Based on two datasets, (i) an original 22-factor sample and (ii) a more comprehensive 187-factor sample, we find that factor momentum effect is weak at the individual factor level. In both samples, only about 22%-27% of the factors exhibit strong return continuation and dominate the factor momentum portfolio while the remaining factors do not. The factor momentum strategies do not outperform the corresponding long-only strategies in either sample. The choice of factors affects the ability of factor momentum to explain individual stock momentum.

Commodity risk in European dairy firms

European Review of Agricultural Economics, 2022

Guillaume Bagnarosa, Mark Cummins, Michael Dowling, Fearghal Kearney

We apply a multivariate mixed-data sampling (MIDAS) conditional quantile regression technique to understand the dairy commodity exposure of European dairy firms. Leveraging a theoretically sound hedonic dairy pricing framework, we show our approach is able to identify both market and operational risk. Profit margins for butter and milk price are particularly important for operational performance. Additional tests are provided, including an application of MIDAS quantile on a period of amplified dairy market risk. Our approach thus allows dairy firms to gain new perspectives on the significant risks posed by the current structure of dairy production in Europe.

Detecting Political Event Risk In The Option Market

Journal of Banking & Finance, 2022

Alexandros Kostakis, Liangyi Mu, Yoichi Otsubo

This study shows that the option market can ex ante detect and quantify the effects of political event risk. Focussing on the 2016 UK referendum on EU membership, we find that the Risk-Neutral Distribution extracted from GBPUSD futures options whose expiry spans the referendum date becomes bimodal and the Implied Volatility curve exhibits an unusual W-shape. To the contrary, the corresponding effects for FTSE100 are found to be very limited. The large swings in expectations regarding the event outcome during the referendum night allow us to observe the counterfactual and validate the ex ante information revealed in the option market.

Direction-of-change forecasting in commodity futures markets

International Review of Financial Analysis, 2021

Jiadong Liu, Fotis Papailias, Barry Quinn

This paper examines direction-of-change predictability in commodity futures markets using a variety of binary probabilistic techniques. As well as traditional techniques, we apply Variable Length Markov Chain (VLMC) analysis, an innovative technique popularised in computational biology when predicting DNA sequences (Buhlmann & Wyner, 1999). To the best of our knowledge, this is the first application of VLMC in finance. Our results show that both VLMC and technical analysis methods provide strong predictability of the direction-of-change of commodity returns, with annualised mean returns of approximately 8%, substantially higher than the passive long strategy. Our results suggest that a short-term learning effect is present in commodities market which can be exploited using innovative direction-of-change forecasting techniques.

Dividend or growth funds: what drives individual investors' choices?

International Review of Financial Analysis, 2021

Dun Han, Liyan Han, Yanran Wu, Pei Liu

We study dividend fund buying behavior using over 80,000 individual Chinese mutual fund investors from a private Chinese mutual fund account dataset. Based on a variety of specifications and logistic regressions, we empirically investigate investors' characteristics in choosing dividend-paying and/or growth mutual funds under different market scenarios. To the best of our knowledge, this research represents an initial attempt to study individual dividend investors in mutual fund markets. We find that older Chinese investors prefer dividend-paying funds less than growth funds, but this depends on different market conditions, and the age effect shows a nonlinear mode when considering age grouping. Moreover, investors' prior experience plays a crucial role in choosing the fund type; however, the conclusions vary with market scenarios. In addition, female investors prefer more dividend-paying funds than do male investors, but investing experience counteracts this difference. We also find that geographic location is a contributor when investors decide the fund type.

Return signal momentum

Journal of Banking & Finance, 2021

Fotis Papailias, Jiadong Liu, Dimtrios D. Thomakos

A new type of momentum based on the signs of past returns is introduced. This momentum is driven primarily by sign dependence, which is positively related to average return and negatively related to return volatility. An empirical application using a universe of commodity and financial futures offers supporting evidence for the existence of such momentum. Investment strategies based on return signal momentum result in higher returns and Sharpe ratios and lower drawdown relative to time series momentum and other benchmark strategies. Overall, return signal momentum can benefit investors as an effective strategy for speculation and hedging.

Infographics by Topic