QUB Finance Research

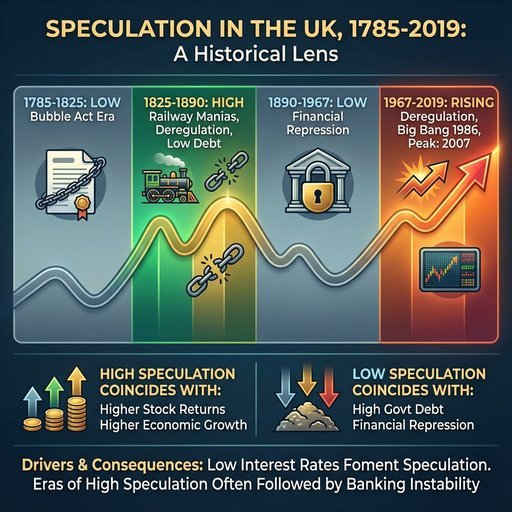

Speculation in the UK, 1785-2019

Economic History Review, 2025

William Quinn; Clive B. Walker; John D. Turner

Speculation has long been thought to have significant economic effects, but it is difficult to measure, making it challenging to examine these effects empirically. In this paper we measure speculation in the UK since 1785 by using business and financial reporting in The Times newspaper. Our monthly speculation index reveals four distinct epochs of speculation in the UK. Epochs of high speculation coincide with higher stock market returns and higher economic growth, while low speculation periods coincide with high levels of government debt and financial repression. We find that low interest rates foment the development of higher speculation, and that eras of higher speculation are often followed by greater banking instability.

Liquidity and Price Informativeness of Options: Evidence From Extended Trading Hours

Journal of Futures Markets, 2025

Liangyi Mu, Arie E. Gozluklu

This paper explores the trading dynamics of the options market during extended trading hours (ETHs). During ETH, the options market is characterized by low liquidity and decreased trading activities, yet there is an increased likelihood of informed trading. The introduction of ETH improves overall market liquidity on the following trading day, as reflected by a reduction in the quoted and effective bid–ask spreads, for both index options and their underlying constituents. The improvement of liquidity is due to the timely incorporation of overnight news into option prices during ETH. Moreover, option prices during ETH are informative for the index level and realized volatility in the subsequent regular trading hours.

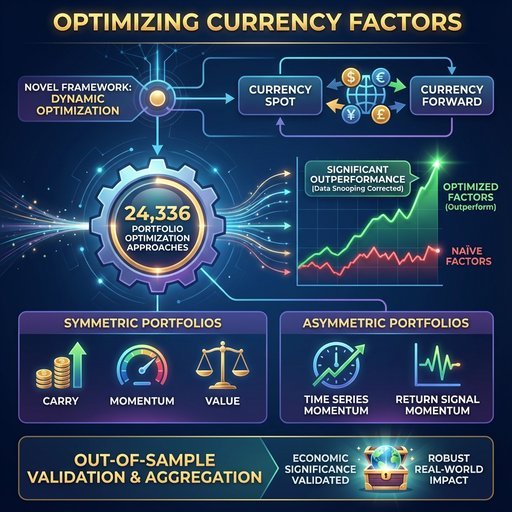

Optimizing Currency Factors

Financial Review, 2025

Minyou Fan, Fearghal Kearney, Youwei Li, Jiadong Liu

We introduce a novel framework that dynamically optimizes currency factor strategies via trading currency spot and forward. We examine the performance of 24,336 portfolio optimization approaches and find that the optimized currency factors significantly outperform the naïve factors after correcting for data snooping bias. Our framework suits both symmetric factor portfolios, including carry, momentum, and value, and asymmetric factor portfolios, such as time series momentum and return signal momentum. An out-of-sample procedure that aggregates all the outperforming optimization approaches validates the economicsignificance of our optimized factor portfolio.

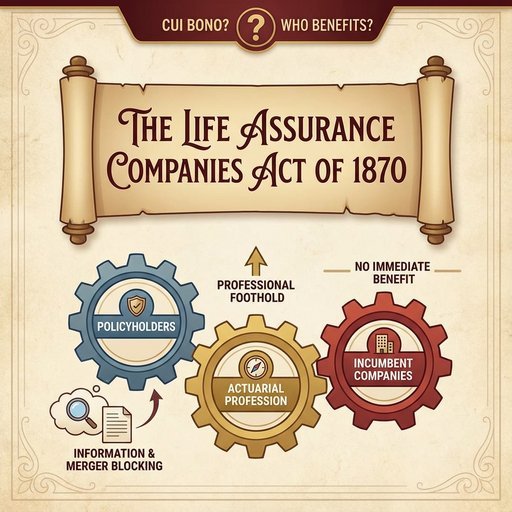

The introduction of financial services regulation in Britain in 1870: cui bono?

Business History, 2025

David A. Bogle

Who benefits from the introduction of regulation of financial services? This article addresses this question by looking at the introduction of one of the first pieces of UK financial services regulation, the Life Assurance Companies Act of 1870 (‘the 1870 Act’). The evidence suggests that, although the policyholders and the actuarial profession obtained some benefits from the 1870 Act, the shareholders of incumbent life assurance companies did not, at least not immediately nor directly. The policyholders benefitted from the ability to block mergers occurring and the increased information about life assurance companies that was made available to them. The actuarial profession, whilst not getting everything they requested from the 1870 Act, used it as a launching pad to obtain a stronger foothold in the life assurance industry.

Unravelling the volume-volatility nexus in cryptos under structural breaks using fat-tailed distributions: mixture of distribution hypothesis and implications for market efficiency

European Journal of Finance, 2025

Saswat Patra; Neha Gupta

The study examines the relationship between volume and volatility in leading cryptocurrencies i.e. Bitcoin and Ethereum, within the framework of Mixture of Distribution Hypothesis (MDH). It accommodates structural shifts in the cryptocurrency prices and uses fat-tailed distributions. The results show that the MDH is rejected for both cryptocurrencies, and volume alone cannot explain the heteroskedasticity of returns; however, it acts as a significant predictor for volatility, especially when incorporating structural breaks in the model. Further, the forecasting performance improves when fat-tailed distributions, such as the skewed student’s t and Johnson’s Su distribution are used to model the innovations. Thus, volume holds important information in the crypto markets and can affect returns, thereby, raising concerns about market efficiency. Our results are robust across different periods, modelling approaches and forecasting horizons, and hold substantial implications for traders, market participants, regulators, and governments in designing effective policies.

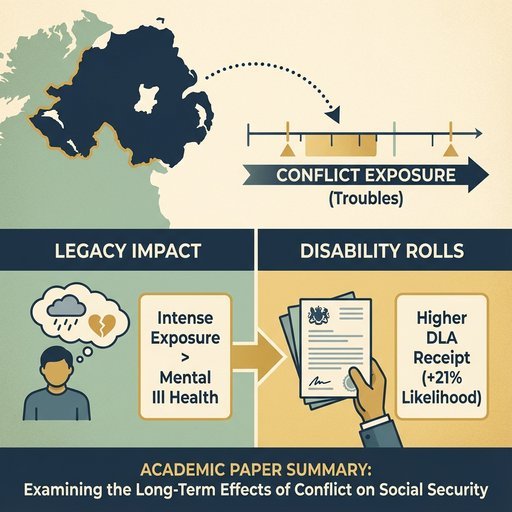

The legacy of the Northern Irish 'Troubles' on Disability Rolls

Social Science & Medicine, 2025

Anne Devlin; Declan French; Duncan McVicar

Disability benefit recipiency rates have been persistently higher in Northern Ireland (NI) than the rest of the UK for decades. Receipt of Disability Living Allowance (DLA), a social security payment designed to cover the additional costs of living with a disability, was proportionally around twice as high in NI compared to the rest of the UK at its 2016 peak. This paper uses data from the Northern Ireland Cohort of Longitudinal Ageing survey to examine whether one potential contributory factor, exposure to the conflict, can explain variations in DLA receipt among older working-age people in Northern Ireland. Conflict-related fatality rates at the area level are used to account for potential endogeneity in reporting past exposure to trauma. While most of the NI population in the age bracket examined (50-64 years) were exposed to the conflict in some way, more intense exposure to the conflict is found to increase the likelihood of DLA receipt by 21 percentage points. We also find a substantial impact on mental ill health. This research has significant policy ramifications both in NI but also across the UK at a time of particular interest in disability benefit receipt as well as contributing to the wider post-conflict literature.

Green innovation optimization for climate change ESG business readiness: role of generative AI in BRICS countries

European Financial Management, 2025

Noman Arshed; Yassine Bakkar; Marco De Sisto; Mubbasher Munir; Shajara Ul-Durar

Climate change introduces new challenges for businesses which require them to find ways to be resilient. Green innovations contribute to boost Environmental, Social, and Governance (ESG)-readiness leading to just transition without optimization. This study estimates the nonlinear effect of environmental innovation in ESG-readiness against climate change while allowing for the moderating role of citations from regenerative AI-research. We use BRICS countries to conduct the analyses with a machine learning based Panel-QARDL. We find that green innovations trace an inverted U-shaped effect and generative AI shifts this relationship upwards. Findings highlight the role of regenerative AI in boosting green innovation performance.

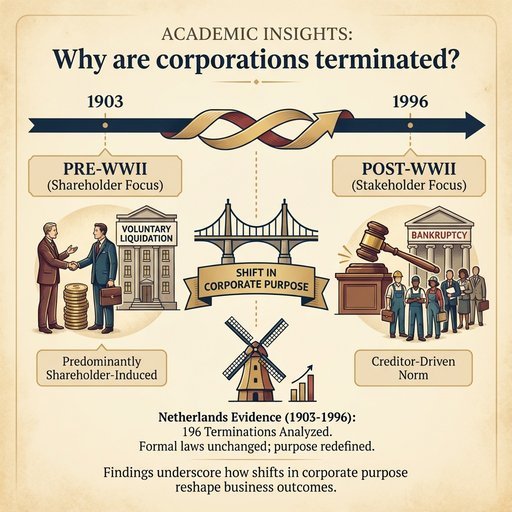

Why are corporations terminated? A century of evidence from the Netherlands

Business History, 2025

Christopher L. Colvin , Abe de Jong, Philip T. Fliers and Florian Madertoner

We identify all 196 Dutch exchange-listed corporations that halted their operations and ceased to exist between 1903 and 1996. We then explain these terminations using unique hand-collected accounting and governance data and regression techniques suited to long-run comparative analysis. Although Dutch bankruptcy laws remained unchanged across the twentieth century, patterns of corporate exit shifted markedly: shareholder-induced voluntary liquidations predominated before WWII, while creditor-driven bankruptcies became the norm thereafter. Our analyses suggest this transformation reflected a broader redefinition of corporate purpose, from a liberal shareholder-centric model before WWII, to a stakeholder-focused paradigm that emerged among Dutch business leaders in the post-war period. We further find that the Dutch government’s industrial policy initiatives in the 1970s did not succeed in reducing corporate failures. Our findings underscore how shifts in corporate purpose can fundamentally reshape business outcomes, even in the absence of formal legal changes.

On the origin of green finance policies

Journal of Financial Stability, 2025

T.F. Cojoianu, D. French, A.G.F. Hoepner, L. Sheenan

Despite the rising number of green finance policies, the socioeconomic determinants shaping them remain largely unexamined. Drawing from the literature analysing the relationship between regulation, market development and institutional economics, we contend that green finance policy adoption is driven by both market based and institutional factors. Using a survival analysis approach to understand the levers influencing green finance policy adoption across 188 countries from 2000 to 2019, we find that exposure to the fossil fuel industry predominantly drives the initial issuance of green finance policies. The positive effect of fossil fuel commercial financing on the adoption of green finance policies exists in countries with high and medium climate change awareness levels. Meanwhile, in countries with a low climate change awareness level, fossil fuel government subsidies drive green finance policy adoption. Our study also highlights the role of the financial industry as one of the key actors in the policy cycle of green finance policies via two pathways: (i) affecting financial stability through financing oil and gas companies on primary financial markets and (ii) developing a market for sustainable finance products.

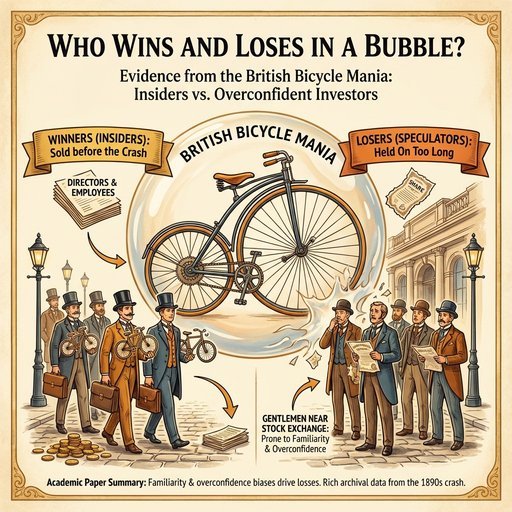

Who Wins and Loses in a Bubble? Evidence from the British Bicycle Mania

Journal of Economic History, 2025

William Quinn and John D. Turner

How do different types of investors perform during financial bubbles? Using a rich archival source, we explore investor performance during the British bicycle mania of the 1890s. We find that directors and employees of cycle companies reduced their holdings substantially during the crash. Those holding shares after the crash were generally not from groups stereotypically thought of as naïve, but gentlemen living near a stock exchange, who had sufficient time, money, and opportunity to engage in speculation. Our findings suggest that the investors most at risk of losing during a bubble are those prone to familiarity and overconfidence biases.

Understanding the Performance of Currency Basis‐Momentum

European Financial Management, 2025

Minyou Fan, Xing Han, Ang Li, Jiadong Liu

We conduct an in‐depth analysis of basis momentum (BM) in currency markets and examine its relationship with key market anomalies. We find that BM strategies generate significant excess returns across various formation periods. These abnormal returns are not fully explained by the closely related carry and momentum factors. By decomposing the BM signal, we show that both carry‐ and momentum‐related components contribute to the returns of BM strategies. Compared to carry trade, BM strategies exhibit significantly lower risk, leading to superior risk‐adjusted performance.

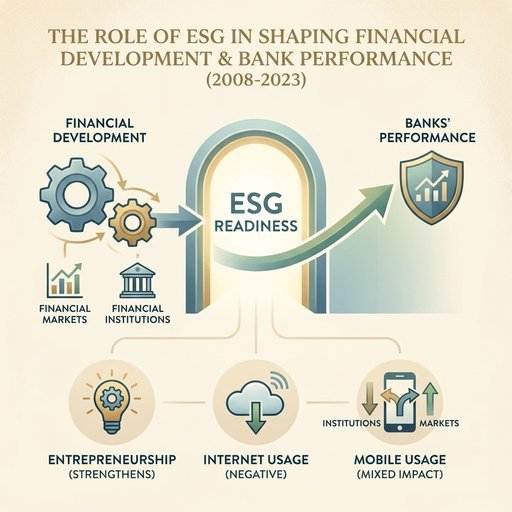

The role of ESG in shaping the impact of financial development on banks' performance

European Financial Management, 2025

Noman Arshed; Yassine Bakkar; Marco De Sisto; Mubasher Iqbal; Shajara Ul-Durar

This study investigates how financial development, divided into financial markets and financial institutions, affects banks' performance across 93 financially developed countries during the period between 2008 and 2023. The analysis highlights the role of environmental, social and governance readiness as core determinants that reshape financial progress and banking outcomes. On the basis of financial intermediation theory and the broader idea of stakeholder engagement, this study finds that entrepreneurship strengthens bank performance, internet usage negatively affects it, and mobile usage shows a negative effect in the case of financial institutions but a positive impact when financial markets are considered.

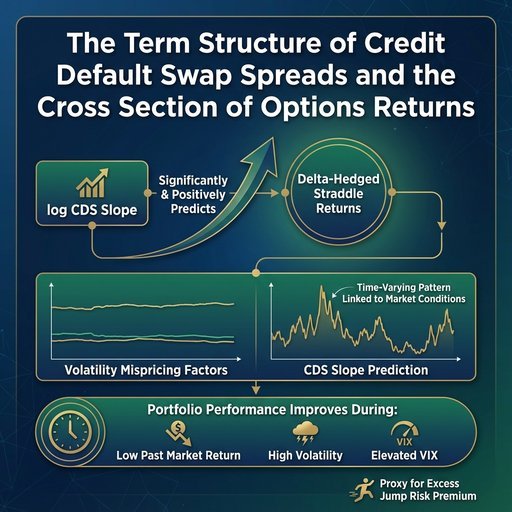

The Term Structure of Credit Default Swap Spreads and the Cross Section of Options Returns

Journal of Futures Markets, 2025

Hao Zhang, Yukun Shi, Dun Han, Pei Liu, Yaofei Xu

This paper, using the natural logarithmic form credit default swap (log CDS) slope, examines the variation in cross‐sectional 1‐month ATM delta‐hedged straddle returns. Our analysis reveals that the log CDS slope significantly and positively predicts these returns, even when accounting for several key volatility mispricing factors. Further investigation shows that this predictive relationship exhibits a strong time‐varying pattern, closely linked to market conditions. In contrast, the relationship between notable volatility mispricing factors and straddle returns remains relatively stable over time. Constructing a long‐short quintile portfolio on straddle options confirms that trading performance improves when the past 12‐month market return is at a historically lower level, market volatility is at a historically higher level, and the VIX is elevated. Log CDS slope, as a proxy for excess jump risk premium, significantly predicts delta‐hedged option returns during periods of high volatility.

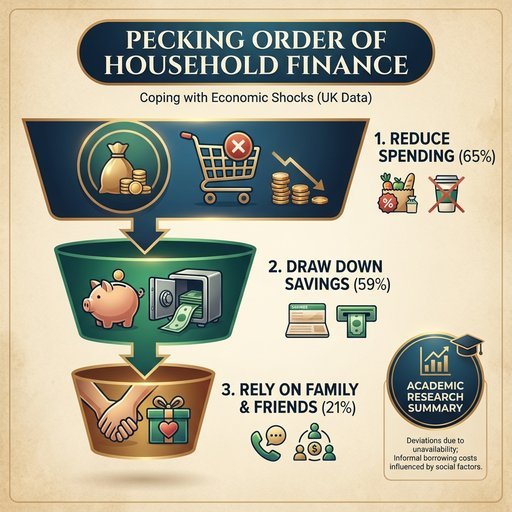

A pecking order of household finance

Oxford Economic Papers, 2025

Declan French

How do households cope with economic shocks? In this article, I provide empirical evidence and theoretical grounding for a pecking order of coping methods using data from the UK Understanding Society COVID-19 Study. I find that there is a typical household finance ordering of responses to income loss. Almost two-thirds (65 per cent) of households first reduce spending then these households typically proceed to draw down savings (59 per cent) and their most common next response is relying on family and friends (21 per cent). Deviations from this ordering occur because certain coping methods are of ten unavailable—those households not reducing spending are already struggling and those without savings have nothing to drawdown. Receiving financial assistance from family and friends is also more common than some authors suggest. Lastly, I find that the costs of informal borrowing are influenced by plausible social factors. My results are informative for policies to promote resilience during crises.

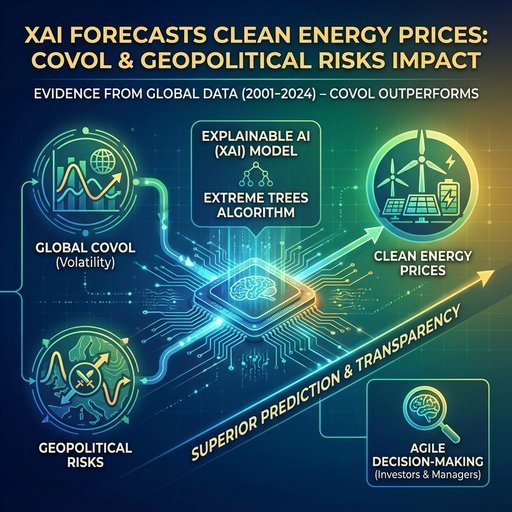

Do global COVOL and geopolitical risks affect clean energy prices? Evidence from explainable artificial intelligence models

Energy Economics, 2025

Sami Ben Jabeur, Yassine Bakkar, Oguzhan Cepni

We investigate the impact of global common volatility and geopolitical risks on clean energy prices. Our study utilizes daily data from January 1, 2001, to March 18, 2024. Using a new framework based on explainable artificial intelligence (XAI) methods, our findings demonstrate that the COVOL index outperforms the geopolitical risk index in accurately predicting clean energy prices. Furthermore, the Extreme Trees algorithm shows superior performance compared to traditional regression techniques. Our findings indicate that XAI improves transparency, thereby making a substantial contribution to agile decision-making in predicting clean energy prices. Practitioners, including investors and portfolio managers, can enhance investment decisions and manage systemic risks by incorporating COVOL into their risk assessment and asset allocation models.

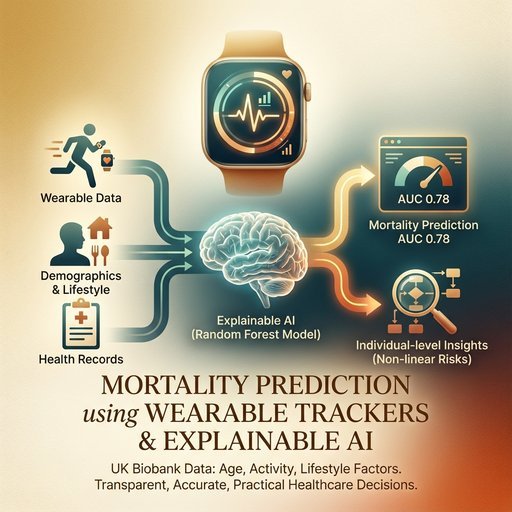

Mortality prediction using data from wearable activity trackers and individual characteristics: An explainable artificial intelligence approach

Expert Systems with Applications, 2025

Byron Graham, Mark Farrell

Mortality prediction plays a crucial role in healthcare by supporting informed decision-making for both public and personal health management. This study uses novel data sources such as wearable activity tracking devices, combined with explainable artificial intelligence methods, to enhance the accuracy and interpretability of mortality predictions. By using data from the UK Biobank—specifically wrist-worn accelerometer data, hospital records, and various demographic and lifestyle factors, and health-related factors—this research uncovers new insights into the predictors of mortality. Explainable artificial intelligence techniques are employed to make the models’ predictions more transparent and understandable, thereby improving their practical applications in healthcare decisions. Our analysis shows that random forest models achieve the highest prediction accuracy, with an area under the curve score of 0.78. Key predictors of mortality include age, physical activity levels captured by accelerometers, and other health and lifestyle factors. The study also identifies non-linear relationships between these predictors and mortality, and provides detailed explanations for individual-level predictions, offering deeper insights into risk factors.

Infographics by Topic